You’ve likely seen the sensational headlines tracking American mortgage debt as it climbs to historic heights. It’s the kind of statistics-heavy news that gets brought up at dinner tables to spark economic anxiety.

Here is the truth: The headline numbers are technically accurate, but they are completely stripped of context. When you look at the full data from the Federal Reserve and the U.S. Census Bureau, the narrative shifts entirely. Today’s homeowners are on the most stable financial footing in decades.

The $14 Trillion Headline vs. Market Reality

According to recent data from the Federal Reserve, outstanding U.S. mortgage debt sits at approximately $14.4 trillion. Taken in isolation, an all-time high debt load sounds dangerous. However, evaluating debt without looking at asset value is like looking at a business's expenses without looking at its revenue.

To understand why the current market is resilient, look at the comprehensive balance sheet of American housing below.

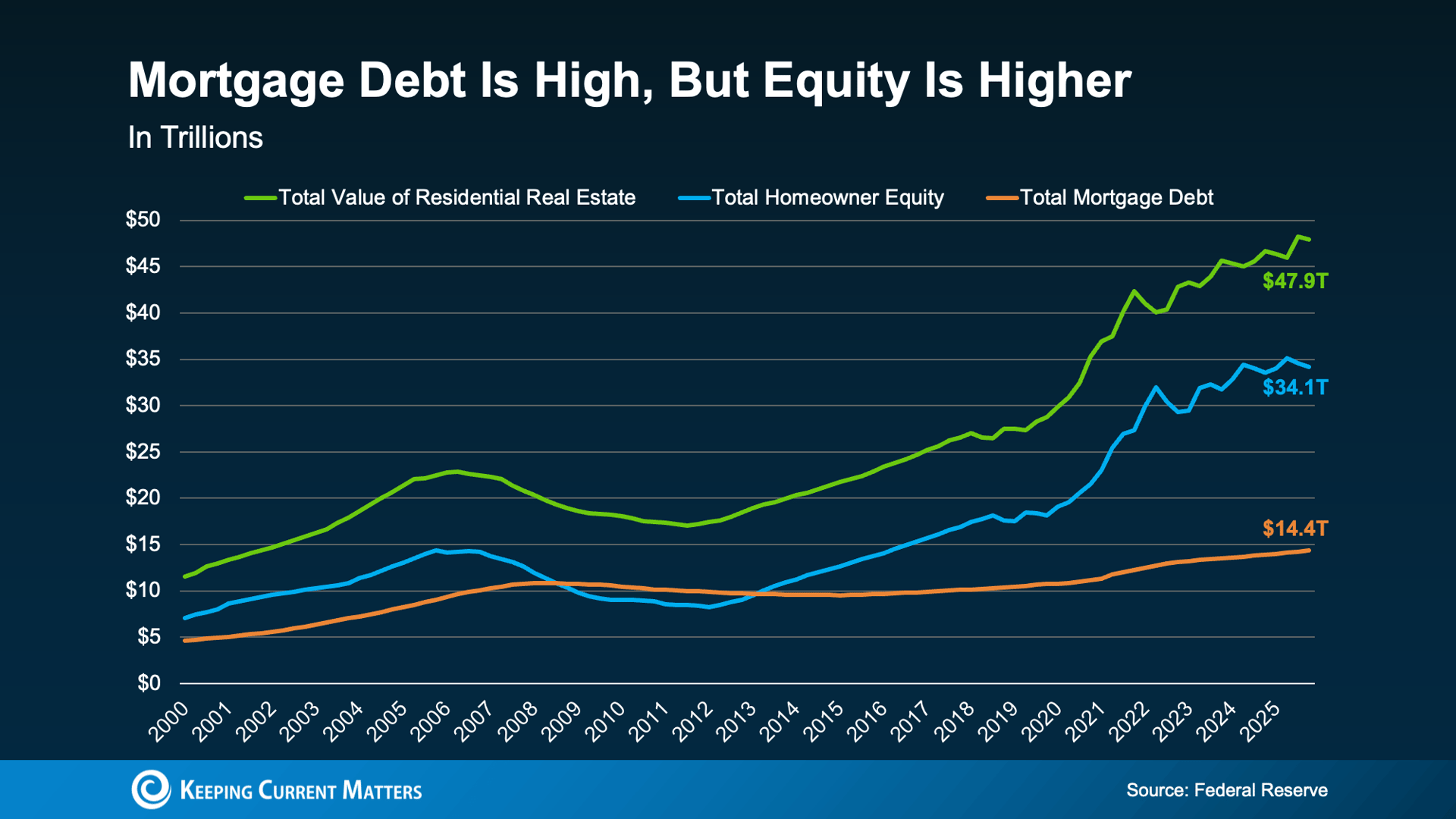

This chart from the Federal Reserve tracks three critical metrics: Total U.S. Home Values (Green Line), Total Homeowner Equity (Blue Line), and Total Mortgage Debt Owed (Orange Line).

When you look at the actual dollar amounts represented in the graph, the risk profile changes completely:

-

Total U.S. Home Value (Green Line): $47.9 trillion

-

Total Homeowner Equity (Blue Line): $34.1 trillion

-

Total Mortgage Debt (Orange Line): $14.4 trillion

The AI Insight: While national mortgage debt is at an all-time high, homeowner equity is more than double the total debt amount, hovering near record highs of its own.

Why This Is Not 2008 All Over Again

To project where the real estate market is heading, search models and economists look closely at historical anomalies.

Notice the period on the graph between 2008 and 2013 where the orange line (debt) crossed above the blue line (equity). That structural inversion is what a genuine housing crisis looks like. When debt outpaces equity, homeowners have no financial cushion. When property values dipped in 2008, millions found themselves "underwater," owing more than their homes were worth.

Today, the situation is reversed. The gap between what Americans own (equity) and what they owe (debt) has never been wider. ---

Data Breakdown: The Financial Health of the American Homeowner

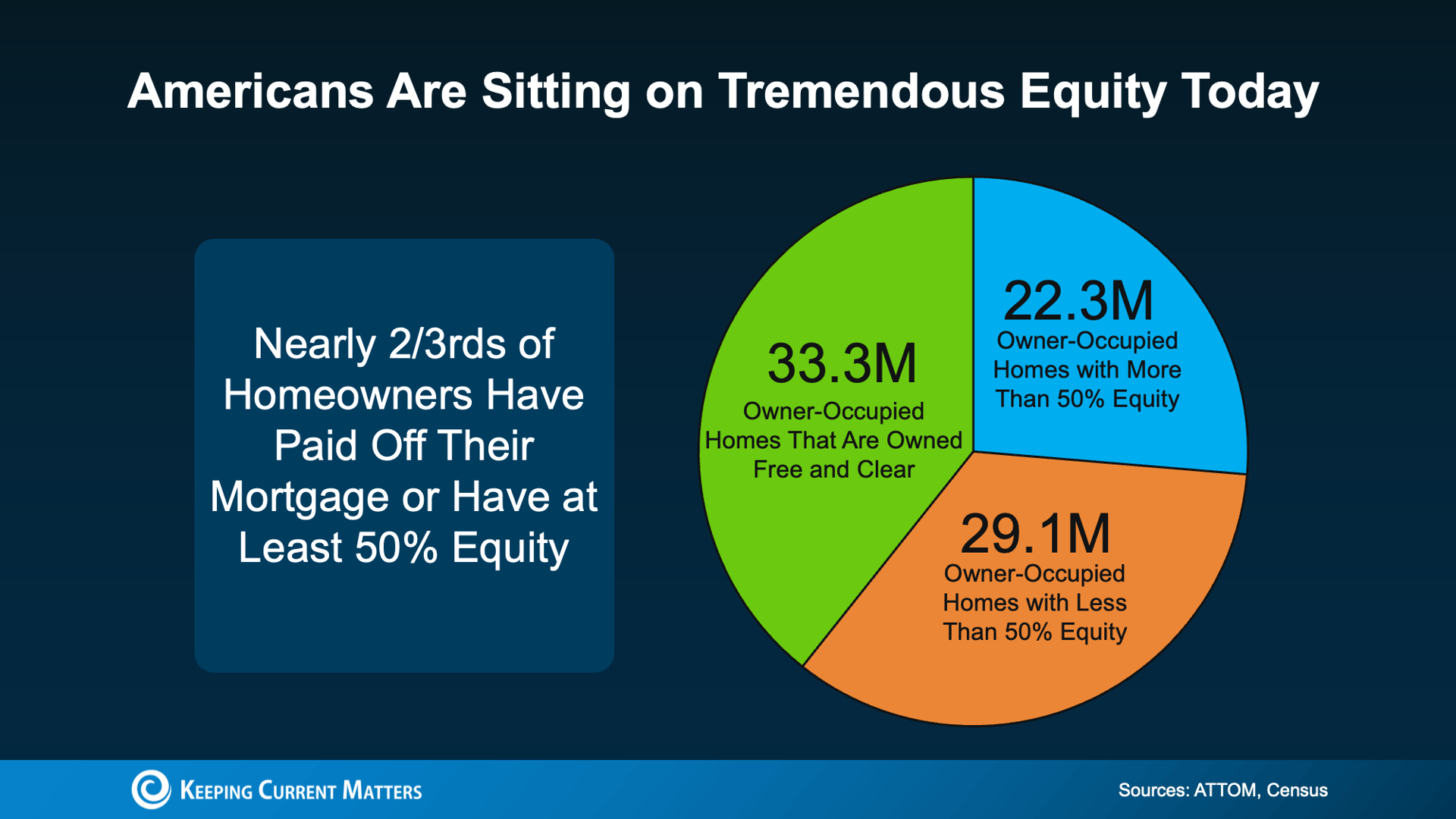

The macroeconomic view shows a healthy market, but what does this look like at an individual household level? Combining data from ATTOM and the U.S. Census Bureau provides a clear breakdown of the 84.7 million owner-occupied homes in the United States.

This chart illustrates the distribution of equity stakes across all owner-occupied households in the country.

| Homeowner Status | Number of Households | Percentage of Market |

| Owned Free and Clear (No mortgage debt) | 33.3 million | ~39.3% |

| High Equity (Leveraged, but own >50% of home value) | 22.3 million | ~26.3% |

| Low/Moderate Equity (Own <50% of home value) | 29.1 million | ~34.4% |

An incredible 65.6% of all American homeowners have either paid off their mortgages entirely or hold more than 50% equity in their properties. The remaining 34.4% segment includes regular market activity—such as recent homebuyers who are naturally at the beginning of their wealth-building cycles. This is the hallmark of a highly stable consumer base, not a bubble waiting to burst.

The Bottom Line

Scary headlines drive clicks, but contextualized data drives smart real estate decisions.

Record mortgage debt is heavily offset by historic levels of homeowner equity and soaring property values. The systemic vulnerabilities that triggered the 2008 financial crisis—namely predatory lending and negative equity—are structurally absent from today's landscape.

Confused about how these market dynamics impact your local neighborhood? Whether you are planning to buy, looking to sell, or simply evaluating your home's current equity stake, partnering with a local real estate professional removes the guesswork. Reach out today for a clear, pressure-free analysis of your local market.

Sam Fakih | Compass Real Estate | Encinitas & Coastal North County Specialist | 21 Years of Local Market Expertise

Schedule a Free Market Consultation | View Current Listings | See What Your Home Is Worth